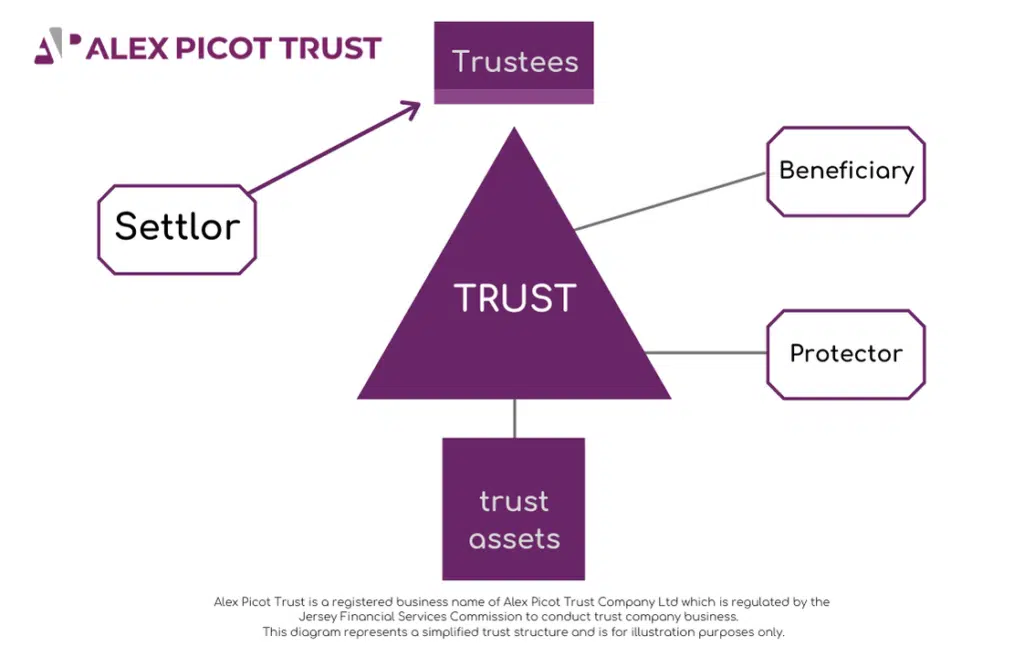

Income Tax

In the previous part in our Offshore Trusts series we considered the UK income tax and capital gains tax treatment of settlor-interested offshore trusts. In this fourth part of our series we consider the income tax treatment of non-settlor interested, or beneficiary-taxed, offshore trusts.

This is part 4 of our Offshore Trusts blog series, written by our Senior Tax Manager Lawrence Adair. Read part one here: ‘All you need to know about Offshore Trusts’ . Read part two here: ‘Residence Positions and Offshore Trusts’ Read part three here: ‘Settlor-Interested Offshore Trusts’

Income tax on beneficiary-taxed offshore trusts – trustee position on UK income

UK income received by a beneficiary-taxed offshore trust is initially taxable on the trustees at a rate depending on the type of trust and income source. As noted in the first of our series, trusts can either be on a discretionary or life interest basis. The initial rate of income tax for each type is:

Discretionary: up to 45% depending on the income source

Life interest: up to 20% depending on the income source

Income tax on beneficiary-taxed offshore trusts – trustee position on non-UK income

Unlike UK income, non-UK income received by a beneficiary-taxed offshore trust is not taxable on the trustees.

Income tax on beneficiary-taxed offshore trusts – beneficiary position generally

How a beneficiary of a beneficiary-taxed offshore trust is taxed depends on the type of trust and their residence.

Income tax on beneficiary-taxed offshore trusts – beneficiary position for discretionary trusts

A beneficiary of a discretionary offshore trust is taxed in the UK according to income distributions received; with the situs of the income being non-UK.

If the beneficiary is non-UK resident they are not taxable in the UK on income distributions received. But may be able to claim repayment of any UK income tax paid by the trustees.

A UK resident beneficiary, on the other hand, is taxed at up to 45% depending on their income levels. With credit given for the UK tax paid by the trustees (provided the trustees are fully UK tax compliant). As well as income distributions; it is possible for payments which are capital in nature to be matched to foreign source income where broadly there was a UK tax avoidance motive in setting up the trust. Capital payments for this purpose include notional payments. Such as low or interest-free loans or low or rent-free use of assets.

As noted in the last part of series, there can be occasions where a settlor is assessable on discretionary distributions of trust income received by their minor children including on all distributions relating to UK source income.

Income tax on beneficiary-taxed offshore trusts – beneficiary position for life interest trusts

A beneficiary of a life interest trust is taxed in the UK according to their share of trust income for each tax year – with the situs of the income being based on the underlying sources. The income assessed on them can include income from underlying offshore companies. Where broadly there was a UK tax avoidance motive in setting up the trust structure.

If the beneficiary is non-UK resident they are only taxable in the UK at up to 45% on UK income sources.

A UK resident beneficiary is taxed on all sources at up to 45% depending on the underlying sources and income levels.

For both non-UK and UK resident beneficiaries a credit is given for the UK tax paid by trustees.

As with discretionary trusts, a settlor will be assessable on UK trust income attributed to their minor children and possibly non-UK income.

UK resident but non-domiciled beneficiaries – remittance basis

A beneficiary tax charge for a UK resident but non-UK domiciled beneficiary is subject to a remittance basis claim for where the distribution is not remitted to the UK. This could be for the entire distribution in the case of a discretionary trust. Or the underlying non-UK sources in the case of a life interest trust.

3 most important points to take away

- One factor affecting UK Income tax for beneficiaries of beneficiary-taxed offshore trusts is the type of trust. For discretionary trusts they are assessed based on distributions received. Whilst, for life interest trusts assessment is based on income as it arises

- Residence status of beneficiaries of beneficiary-taxed offshore trusts impacts the extent to which they are assessable to UK income tax on trust income. A non-UK resident beneficiary is not assessable to the extent of non-UK income. (Which for a discretionary trust is the whole distribution received)

- The settlor of a beneficiary-taxed offshore trust remains assessable to UK income tax for most trust income received by their minor children, particularly UK source income

Written by Lawrence Adair